This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

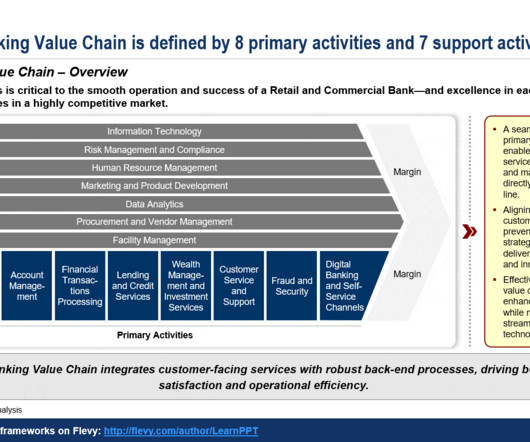

Retail banking is undergoing one of the most significant transformations in its history. As customers shift toward digitalbanking and self-service channels, traditional banks are forced to rethink their value proposition. At the heart of this balancing act is the retail banking value chain.

With the rise of ecommerce sales comes an increase in the use of digital payments and mobile wallets. Next, the bookstore’s payment processor takes the customer’s information and encrypts it so it can securely send it to the customer’s bank, which is the issuing bank. The customer’s bank must authorize the purchase.

Technological Advances : Innovations in AI, machine learning, and digital currencies redefine how organizations operate and meet consumer expectations. Complex Operating Models : Transitioning from traditional to digital-first operations requires agile frameworks that prioritize outcomes over outputs.

Digital payment refers to the electronic transfer of funds or monetary transactions through digital devices such as smartphones, computers, or other connected devices. This includes various methods such as mobile payments, e-wallets, cryptocurrency, online banking, and contactless payments.

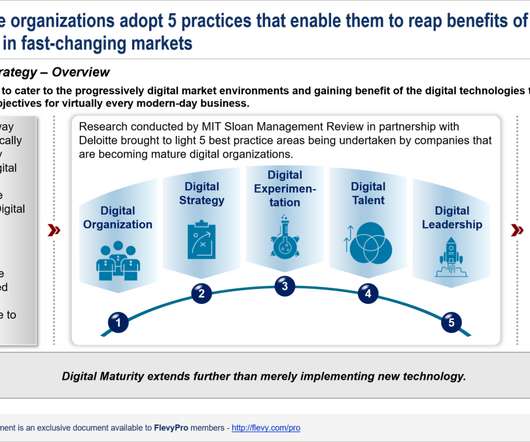

Digital Transformation is a matter of survival now for all organizations particularly businesses. Altering organizations to cater to the progressively digital market environments and gaining benefit of the digital technologies to enhance operations are vital objectives for virtually every modern-day business.

Today, many banks are united by a common challenge: managing the limitations of their legacy cores and the operational, compliance, and customer personalization pitfalls associated with them.

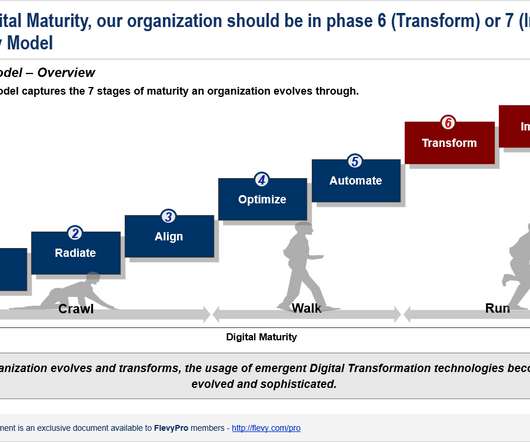

Go digital or go home. To survive in the Digital Age, organizations must pursue Digital Transformation to not only support strategies and reach customers, but also to modernize and achieve excellence in their internal operations and processes. The pursuit of Digital Maturity is quickly becoming a necessity.

The digital world grows larger every day, and it can be hard to keep up. Navigating the ever-changing digital landscape is a challenge — especially if you have a business of your own and are struggling to market yourself and make sales. But you don't have to tackle the trials and tribulations of digital transformation alone.

There are many reasons for even the smallest businesses to have business bank accounts. Plus, come tax time, tracking down expenses and deductions is easier with a business bank account. But depending on the bank, you can also access important services for your company, such as business credit cards and loans. Credit Unions.

UK innovators like Monzo and Revolut have driven digitalbanking forward, prompting traditional banks to adopt similar features. While consumer retail banking may appear saturated, significant opportunities exist in SME, B2B, private, and commercial banking. Source The post So you think digitalbanking is done?

Traditional banks have struggled to get their arms around the new generation of online-only banks and digital financial services that millennials love.

Banks Should Embrace the Opportunities Created by Open Banking The growth of FinTechs and our increased reliance on online payment platforms has led to a sharp rise in digitalbanking services, as more and more customers link their accounts between different providers.

Legacy banks are under pressure from digital-first neobanks that offer convenience and modern services. To stay competitive, traditional banks must embrace digital transformation by adopting AI and mobile-first strategies. However, they face challenges like integrating new technologies with legacy systems and high costs.

Composable banking enhances digital customer experiences by utilizing modular components rather than monolithic systems, allowing financial institutions to quickly adapt to market changes and integrate new services seamlessly. This approach improves operational efficiency, customer engagement, and supports innovation.

As the world grows more and more digital, customers across every industry are expecting digital-first, timely assistance and support. As shown in this digital transformation in banking case study roundup, all businesses — including banks — have been forced to change and evolve with the times.

In today’s digital landscape, banks must continually adapt their digital toolkits to remain competitive and deliver consistently positive customer experiences. AI plays a central role in developing a customer-led culture, allowing banks to prioritize understanding customer needs, preferences, and pain points.

Branch networks are shrinking, and banks need to get better at handling this disruptive process with empathy. One study shows that 31% of customers who switched banks did so when a branch closed. The post The Right Way to Balance Digital and Branch Banking appeared first on NGDATA.

To minimize direct contact, people gravitated towards payment methods that didn't require the use of physical money, like bank cards and payment apps. The Swedish Central Bank recently stated that only 9% of the country's population uses cash for transactions right now. The COVID-19 pandemic is one major catalyst for the shift.

Banks that consistently optimize the customer experience grow 3.2x What is customer experience in banking? Customer experience (CX) in banking is how customers feel about every interaction with your financial service, at all stages of the customer lifecycle. faster than competitors that don’t.

It's the digital age. So why am I, a digital marketer, talking about traditional marketing? The post How banks can lead from the front with digital appeared first on NGDATA. Because we still operate in the physical world. While online consumes much of our daily life, it's not everything—not yet.

Imagine stepping into a world where your banking needs are anticipated before you even voice them, where every interaction feels like a seamless extension of your digital life. This isn’t a distant future but the present reshaping of customer experience (CX) in banking.

Most of the banks has encountered security problems and are looking for a stability. With the advanced digitalbanking, the industry can face different challenges in their security. Artificial intelligence is transformative […]

Recently, I was interviewed by Hannah Wallace from Finextra for my take on the trends in banking in 2021. People of all generations just got used to utilizing digital services faster than we may have predicted a year ago. As a result, banks are faced with expensive.

Banks adopting AI face challenges in training frontline staff. Banks need to address these issues by incentivizing employees to become customers themselves and offering simulation tools and microlearning modules. Source The post Banks May Be Ready for Digital Innovation: Many on the Staff Aren’t appeared first on NGDATA.

With the holiday season in full swing and a global recession predicted sometime in the new year, banks remain committed to investing in modernized technology through digitalbanking transformation efforts vs. traditional cost-cutting routes. “Retail banking customers are expecting more from their banks.

Close the email and leave it to consider later – or worse – toss it in the digital trash bin. Closing Statement 2 Bill, thanks for starting a trial of our HR application for banking. Be so inspired by your email that they contact a competitor that offers similar products or services.

You might be in this situation if you want: Seller protection for digital goods. Skrill allows you to send and receive money, store cards, link bank accounts, and make payments with just your email address and password. Pricing : Pay as you go, $0/month; Bank transfers (ACH), free; Card - Swiped, 2.4% +.25 pay as you go or 1.6%

Banks use real-time client data, AI, cloud computing, and open banking to enhance digital experiences and provide personalized interactions. It also promotes financial inclusion for underserved communities by expanding banking options.

For many of you reading this post, it is quite possible you have already handed someone your digital keys. banks, IP, etc.) Protecting the keys to your digital kingdom is becoming more reliant upon biometric identification, multi-factor authentication (MFA), expanded virtual desktop infrastructure (VDI), and enhanced VPN solutions.

Last month, we attended the Bank Marketing Conference by the American Bankers Association in Austin, which showcased insights, case studies, and networking opportunities. ” The conference covered various topics related to banking marketing strategies, including customer engagement, digital transformation, and brand management.

According to new research , Gartner expects that 80% of B2B sales interactions will occur on digital channels by 2025. Payment processing securely facilitates digital transactions for businesses. A payment processor is the solution that handles these digital transactions for businesses. trillion in 2023.

Banking is an old business. But in the past year, the rapid adoption of financial services innovation technology has catapulted banking, insurance, and financial leaders into the now. Digital Financial Innovation Is The Antidote To Disruption. Check out our top choices, below.

Credit unions have great customer service, but banks excel in digital services. To build and maintain customer loyalty, credit unions must learn from banks and improve their digital offerings. Source The post Banks Have This Major Edge. Can Credit Unions Catch Up? appeared first on NGDATA.

Two years after a pandemic sent more consumers online than ever, 76 percent are now banking on their mobile devices and 82 percent use digital payments – it’s not clear their financial institutions are taking full advantage.

The pandemic has brought upon many digital-first innovations. It has accelerated omnichannel adoption — blending physical and digital commerce channels — as consumers quickly adopt digital-first interactions. We see this pressure mainly coming from digital-first & Source.

Sonata Bank has adopted a niche strategy inspired by the fast-food industry to address the high employee turnover in quick-service restaurants. By providing simple, frictionless banking experiences and leveraging the Digital Onboarding platform, Sonata helps financially underserved employees adopt banking services.

Instead, funds are directly pulled from a customer’s bank account. Automated Clearing House (ACH) Automated Clearing House (ACH) payments are a form of electronic bank transfers. Automated Clearing House (ACH) Automated Clearing House (ACH) payments are a form of electronic bank transfers.

With more people doing business online than ever before, companies are gaining clarity on what’s working and what needs attention when it comes to the digital customer experience. Logging in to websites is part of our daily routines including everything from our banks to our insurance providers […].

It's the digital age. So why am I, a digital marketer, talking about traditional marketing? The post Community banking: A growing alternative appeared first on NGDATA. Because we still operate in the physical world. While online consumes much of our daily life, it's not everything—not yet.

With the growth of digitalbanking, financial institutions should invest in advanced digital experience platforms (DXPs) to better understand and enhance customer engagement. Source The post Don’t Ask Your Bank Customers If They’re Happy. Watch What They Do, Instead. appeared first on NGDATA.

Community banks are increasingly shifting their advertising efforts from social media to streaming platforms like Peacock, Hulu, and Disney Plus. Streaming allows banks to reach broader and more diverse audiences, especially through live sports, which have proven to be highly engaging.

Banks face challenges in managing their legacy cores and personalizing customer experiences. Source The post Blog: The Power of a CDP in BankingDigital Transformations appeared first on NGDATA. Modernizing legacy cores is not a "rip and replace" procedure but can be done in parallel with building mature customer profiles.

Financial institutions need to prioritize their marketing strategies to stay competitive in an increasingly digital world. Source The post Leveling up the bank marketing game appeared first on NGDATA. DCO and social media SEO can also be effective tools.

We organize all of the trending information in your field so you don't have to. Join 105,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content